Global Insights In Depth

Power belongs to those who read between the lines, not just the headlines.

Global Insights In Depth

Power belongs to those who read between the lines, not just the headlines.

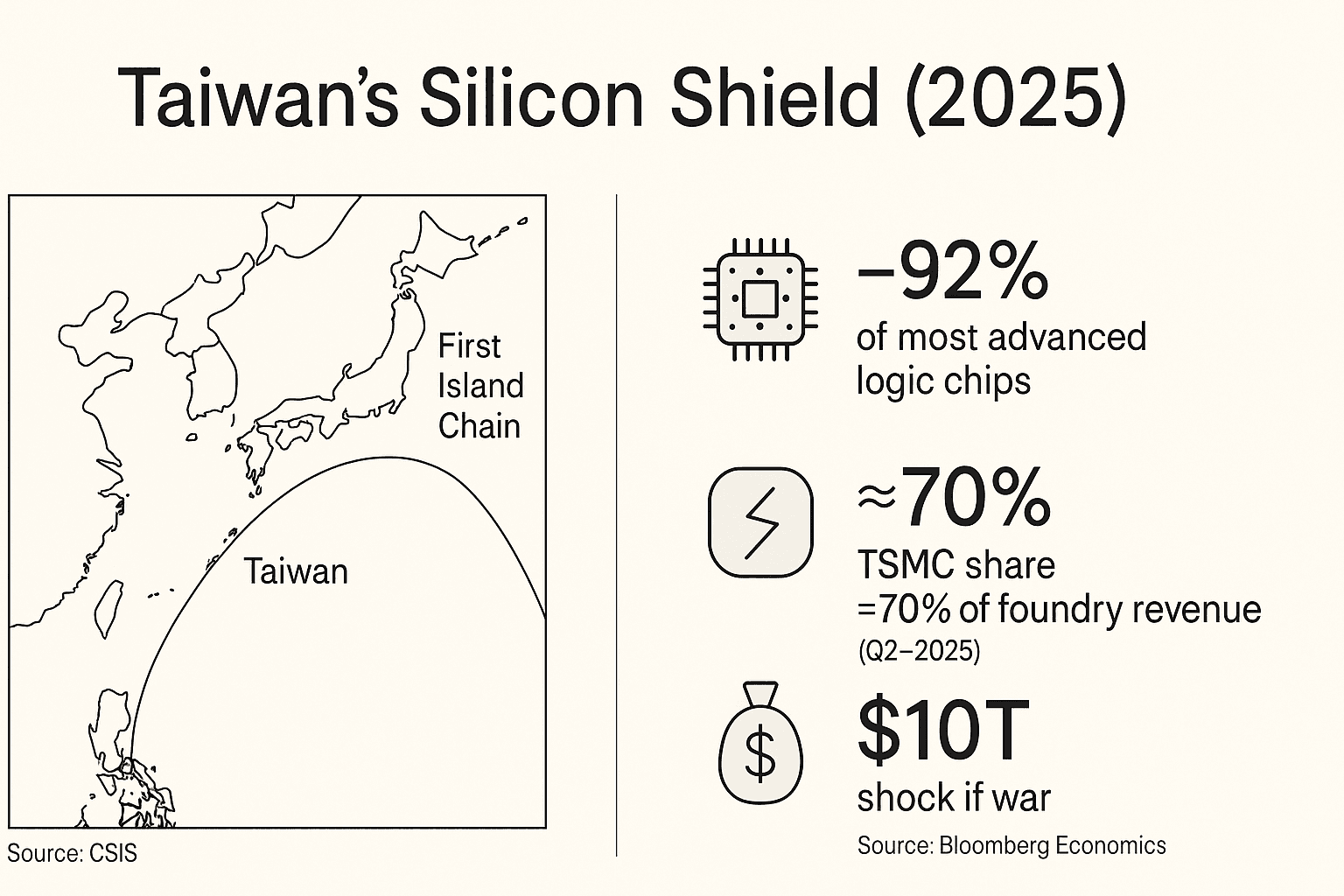

In the world of semiconductors, Taiwan is a titan hiding in plain sight. Despite its small size, Taiwan has become the linchpin of global chip production. As of 2023, the island was responsible for around 20% of total world semiconductor output – but an even more astonishing 92% of the cutting-edge chips (logic chips at 7 nanometers and below) that power advanced electronics. In practice, this means the vast majority of the brain-like processors running our smartphones, laptops, data centers, and AI systems are fabricated in Taiwan. One Taiwanese company in particular – TSMC (Taiwan Semiconductor Manufacturing Co.) – is the unrivaled heavyweight in this space.

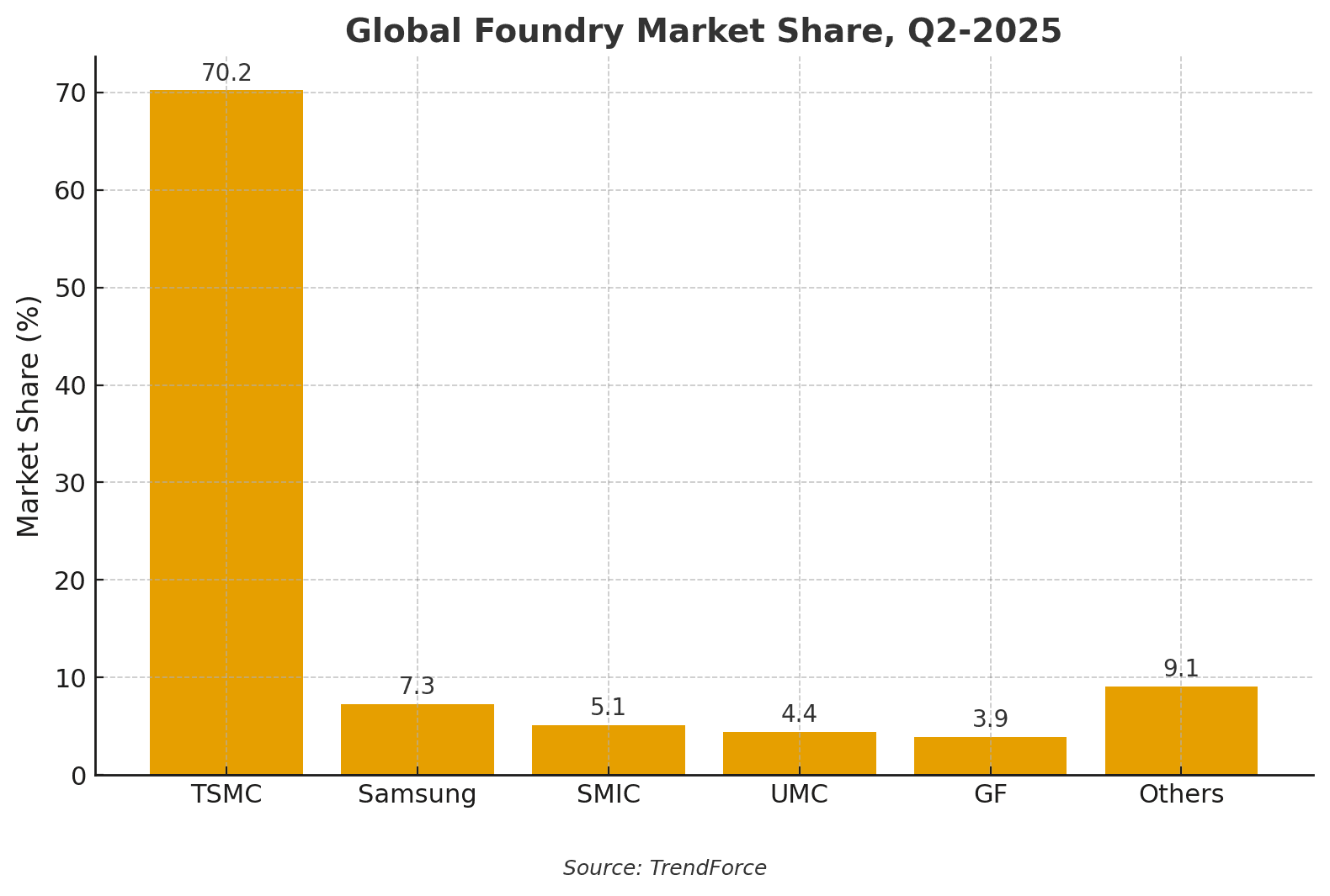

Over the past decade, TSMC has perfected the art of making increasingly tiny and powerful chips, while other contenders fell behind. By 2024, TSMC’s dominance in the contract chipmaking market had grown to 64% of global foundry revenue, up from about 60% a year prior. (By mid-2025, its share hit a record ~70%, widening an already huge lead over competitors in South Korea, China, and the U.S.) This single firm now produces critical components for tech giants worldwide: Apple’s latest iPhone processors, NVIDIA’s AI accelerators, Qualcomm’s 5G chips, and countless others all roll off TSMC’s Taiwanese production lines. Samsung (in South Korea) is a distant second in advanced foundry market share, and no U.S. or European player currently manufactures leading-edge chips at scale.

Every tech company reliant on advanced chips carries an unhedgable Taiwan risk on its balance sheet. If a natural disaster, trade blockade, or conflict shut down Taiwan’s semiconductor industry, the impact would be akin to the oil shocks of the 1970s, but for modern technology. Companies like Apple, NVIDIA, and AMD would have no quick replacement for TSMC’s capacity – potentially halting product lines and R&D pipelines. Automakers learned this the hard way during the 2020-2021 chip shortage, when a lack of certain Taiwanese-made microcontrollers forced car factory shutdowns globally. This reliance has effectively created a “Taiwan premium” – a strategic vulnerability where the world is willing to tolerate higher risk (and potentially higher costs) just to access Taiwan’s unrivaled chips.

Taiwan’s centrality has not gone unnoticed by world powers. Strategists often talk about Taiwan’s “silicon shield.” The idea is that Taiwan’s role is so critical to the global economy that it acts as a protective shield: Beijing might be deterred from invading for fear of destroying the chip infrastructure it also desperately needs, and the U.S. (and other nations) are compelled to defend Taiwan to safeguard the global tech ecosystem. As one researcher put it, the silicon shield exists because “Taiwan has long held over 90% of global advanced chip capacity, which could help deter a Chinese invasion”. In other words, any military aggression would risk shattering the crown jewel of semiconductor production – an outcome catastrophic to all sides.

However, being the keystone of global tech comes with a paradox: Taiwan’s greatest strength is also a source of vulnerability. The island’s dominance makes it a target in great-power rivalry, and its industry’s concentration raises the stakes of even minor disruptions. This reality has thrust Taiwan into the center of a brewing “AI chip war” – a contest that is about far more than just business profits. It’s about technological supremacy, economic security, and geopolitical power in the 21st century.

The explosion of artificial intelligence in recent years has supercharged the strategic importance of semiconductors. Advanced chips are the engines of AI – from training massive language models to powering autonomous vehicles – and whoever controls the best chips holds a key advantage in the AI era. This has accelerated what was already a fierce competition into something of an arms race. And in that race, Taiwan’s role became even more pivotal.

Consider the numbers: in 2024, surging demand for AI-capable chips was a major factor driving TSMC’s growth to 64% market share. Tech companies worldwide scrambled to secure GPUs and AI accelerators for machine learning – notably, NVIDIA’s coveted A100 and H100 graphics processors – and almost all of these are manufactured by TSMC in Taiwan. The AI boom effectively funneled more revenue and influence to Taiwan’s chip sector. By 2025, high-end chip orders for AI data centers, cloud computing, and 5G networks were at record highs, and Taiwan’s semiconductor exports were soaring to meet the appetite.

For China and the United States alike, AI leadership is a national priority, seen as foundational to economic might and military power in the coming decades. Top-tier semiconductors are essential to that leadership. This is why the U.S. has moved to strictly control AI chip technology – for instance, banning the export of cutting-edge NVIDIA and AMD chips to China – and why China has been racing to develop indigenous alternatives. The term “AI chip war” captures this intense rivalry: it’s not a kinetic war, but a competition in R&D labs, fabs, and supply chains to see who can develop and deploy the most advanced processors.

Chips are now often described as “the new oil” or the new nukes in terms of strategic importance. Access to semiconductors determines who can run the fastest supercomputers, train the most advanced AI models, and even build state-of-the-art weapons systems. From autonomous drones to cyber defenses, military applications of AI depend on cutting-edge chips. This lends a national security dimension to what was once mainly a commercial sector. A country that cannot secure high-end chips could find itself lagging in everything from economic productivity to defense capabilities.

It’s in this context that Taiwan’s position is sometimes likened to having the “keys to the future.” If data is the new oil, then Taiwan is sitting on the world’s richest oil field – except the “oil” is the technical expertise and manufacturing capacity to make the most advanced logic chips on Earth. The geopolitical implication is profound: any nation’s AI ambitions can be stymied if its access to Taiwan’s chips is cut off. We’ve already seen early shots of this battle. In 2023, China’s premier telecom giant Huawei surprise-launched a smartphone with a 7nm chip purportedly made in China, an attempt to show it can still innovate under U.S. sanctions. But analysts noted the chip’s production volume and tech origin were limited – highlighting how difficult it is to break free from dependence on Taiwan and Western technology.

In short, the AI revolution has amplified the stakes of the chip war. Taiwan, as the primary producer of the “ammunition” (advanced chips) for that revolution, holds a uniquely powerful position. It’s a position both Beijing and Washington are intensely aware of – and each is strategizing furiously to navigate a future where AI supremacy could well hinge on who can keep Taiwan’s fabs running on their side.

Faced with the reality that so much of the semiconductor supply chain runs through Taiwan (and South Korea to a lesser extent), the United States and its allies have launched an all-out effort to rebalance and secure chip production. The goal is twofold: reduce dependence on Taiwanese chips for critical needs, and prevent China from gaining control of the technologies that Taiwan currently excels in. This has led to a flurry of policy moves, investments, and international agreements since the early 2020s.

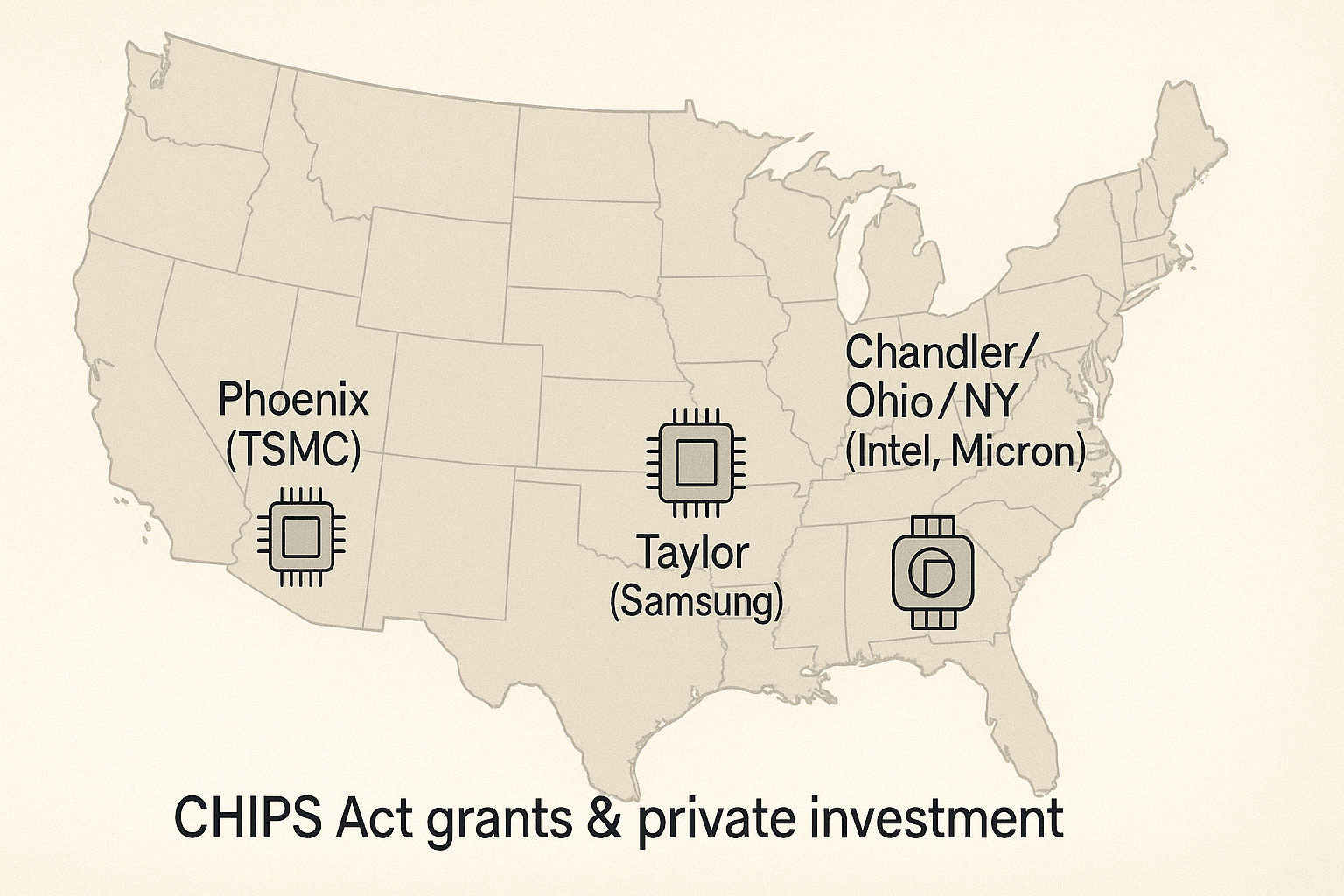

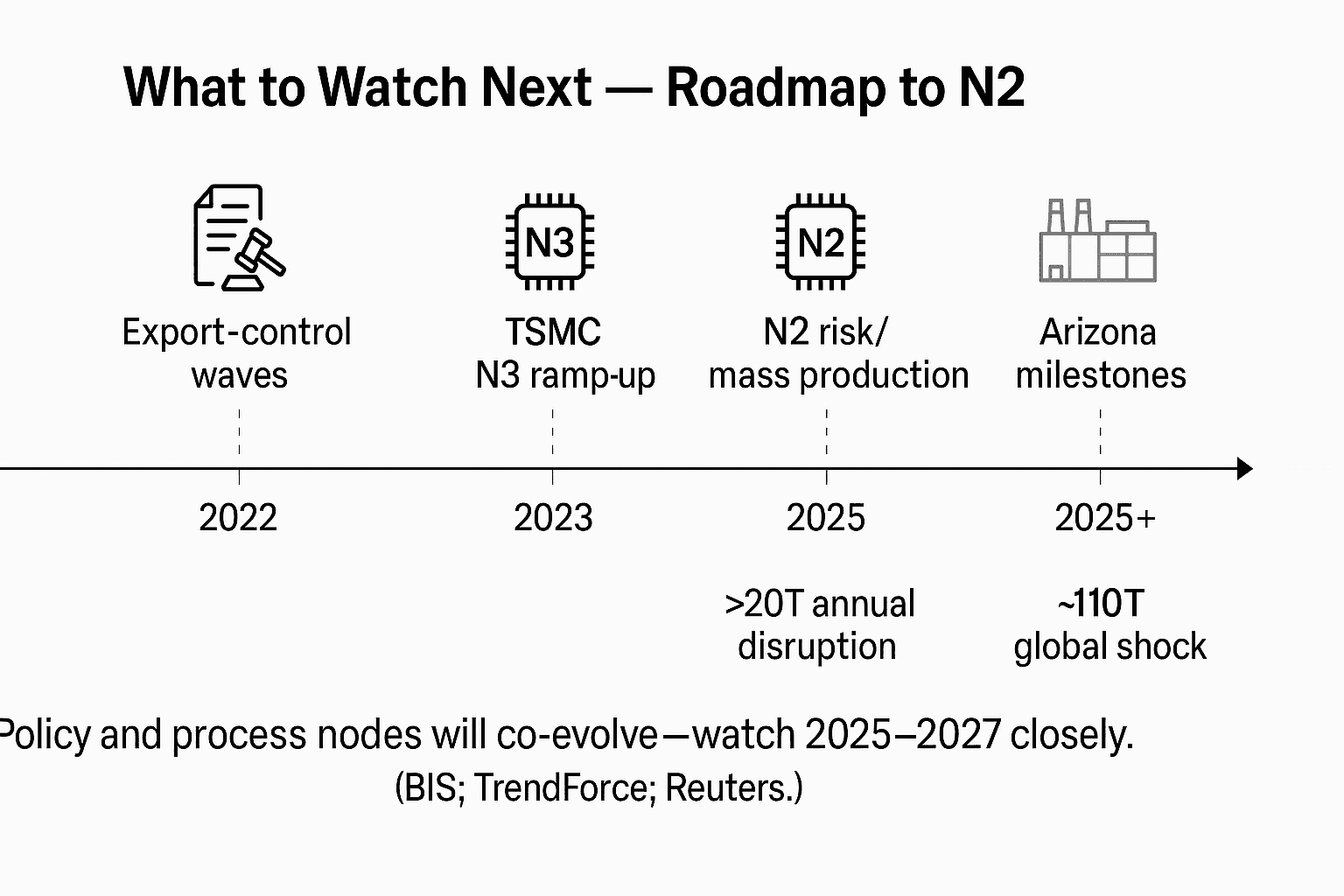

On the home front, the U.S. passed the CHIPS and Science Act in 2022, which earmarked $52 billion in subsidies to jumpstart domestic semiconductor manufacturing and R&D. Crucially, this federal push has catalyzed over $400 billion in private-sector commitments to build new fabs and facilities in America’s tech corridors. Companies have announced dozens of projects: TSMC itself is constructing a massive chip fab complex in Arizona (with the first advanced 4nm production line reportedly starting pilot production in late 2024), Samsung is expanding its Texas foundry, Intel is investing heavily in new fabs in Ohio and Arizona, and Micron and others have plans for memory chip plants. The vision is to onshore a significant chunk of production that today happens in East Asia, thereby safeguarding supply for U.S. industry and military needs.

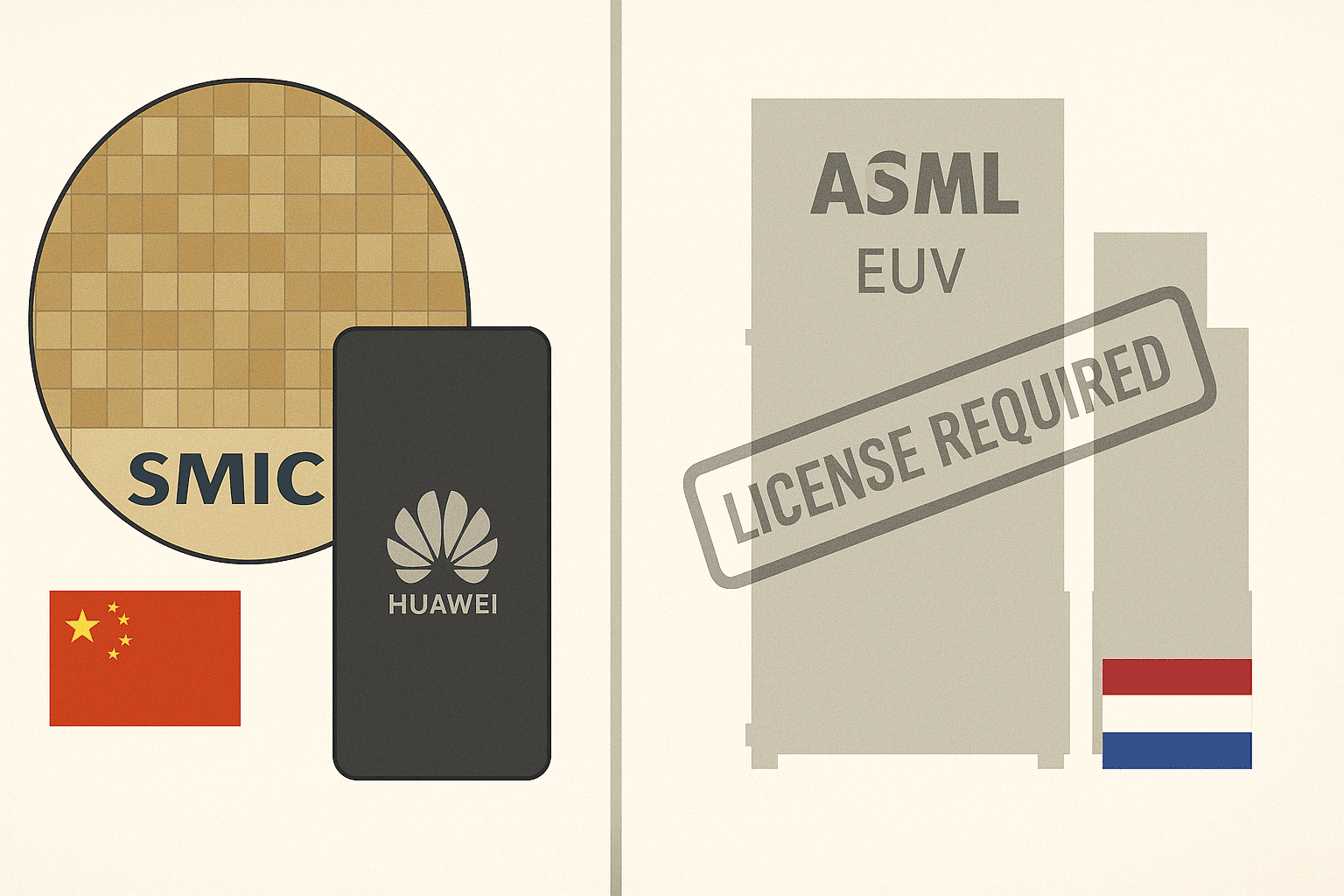

Beyond subsidies, the U.S. has also tightened export controls in coordination with allies. In 2023, Washington updated its rules to ban even more advanced chips and chipmaking tools from being sold to China, closing loopholes in an earlier 2022 ban. Japan and the Netherlands – key players due to companies like Nikon, ASML, and Tokyo Electron – joined these efforts by restricting exports of extreme ultraviolet (EUV) lithography machines and other equipment to China. This effectively chokes off China’s access to the tools required for making the most advanced chips, at least as long as the coalition holds. The strategy here is clear: maintain a technological gap where the U.S. and its partners stay a couple of generations ahead of China in chip tech, partly by denying China the means to catch up, and partly by outpacing them in innovation.

Diplomatically, the U.S. has been shoring up what some call the “Chip Alliance” – closer cooperation among semiconductor powerhouses like Taiwan, South Korea, Japan, and the U.S. There have been high-level dialogues on supply chain security and even proposals for a “Chip 4” alliance to coordinate investments and standards among these players. While formal alliances are nascent, the intent is to bind friendly chip makers together so that, for example, if China tried to cut off one source, alternatives could fill the gap. It’s a kind of collective security arrangement, but for silicon wafers instead of conventional arms.

Taiwan, for its part, has a foot in both worlds – continuing to do the bulk of its manufacturing at home while also carefully acceding to some U.S. requests. TSMC’s move to build fabs in the U.S. is a historic shift; for decades, the company kept its crown-jewel production strictly in Taiwan. Now, under geopolitical pressure, it’s cautiously globalizing a bit. However, TSMC has made it clear that its most advanced technologies will remain in Taiwan for the time being (its Arizona plant will initially produce 4nm and eventually 3nm chips, but its cutting-edge 2nm process is set to debut in Taiwan around 2025-2026). This underscores a key point: even as new plants sprout elsewhere, Taiwan is not standing still. The island is determined to maintain its edge. In 2024, Taiwan’s total semiconductor output value hit a record $165 billion (up 22% from the prior year) amid the global chip boom. The investments by others, though massive, are still playing catch-up to an industry Taiwan has spent over three decades cultivating.

There are also signs of tension within this cooperation. U.S. officials have floated ideas like requiring “50-50” production sharing – essentially urging that half of chips for the U.S. market be produced on American soil. This has been met with some unease in Taipei, which sees such moves as potentially undermining its silicon shield by shifting capacity out of Taiwan. Striking a balance is tricky: the U.S. wants more resilience and less overreliance on Taiwan, but not to the extent that Taiwan’s economy (and deterrence value) is weakened. As of 2025, the working solution seems to be diversification, not decoupling: build backup fabs in the U.S., Japan, and Europe, while still relying on Taiwanese know-how and talent to run many of them.

From an economic perspective, this grand realignment is costly but seen as necessary insurance. The free-market era of offshoring chips for maximum efficiency is giving way to an era of “techno-nationalism,” where nations explicitly plan industrial capacity for strategic reasons. The United States and its allies are effectively racing against the clock – hoping to erect a more distributed semiconductor ecosystem before any crisis knocks Taiwan’s contribution offline. Until then, they remain deeply reliant on that small island’s output, which is why safeguarding Taiwan remains an American priority not just for ideological reasons, but for hard economic and security interests.

On the other side of the chessboard, China is determined to break its dependence on foreign (especially Taiwanese and American) chip technology. President Xi Jinping has explicitly called for achieving “technology self-reliance”, recognizing that semiconductors are a glaring Achilles’ heel in China’s otherwise mighty manufacturing machine. Each year, China imports hundreds of billions of dollars worth of chips – in 2022, it spent more on importing semiconductors than it did on oil. This reality is both an economic liability and a strategic vulnerability for Beijing, one it is spending lavishly to fix.

China’s game plan for chips has several fronts:

Despite these efforts, China faces a stark dilemma. The more it lags in cutting-edge chips, the more its economy and military development could be constrained. Yet the very actions it takes to address this lag (like aggressive industrial policies or saber-rattling over Taiwan) often spur its rivals to double-down on denying China access to the top-tier tech. For example, each time Beijing ramped up pressure on Taiwan or in the South China Sea, it seemingly strengthened Washington’s resolve to tighten the high-tech chokepoint. Likewise, China’s military modernization – which increasingly depends on advanced semiconductors for everything from missiles to AI-driven surveillance – is seen as a direct threat by the West, justifying even more stringent measures to keep the best chips out of Chinese hands.

Taiwan sits uncomfortably at the center of this. From China’s perspective, acquiring Taiwan (which it considers a renegade province) could, in theory, instantly hand it the world’s leading chip fabs and know-how. This is one reason Taiwan’s semiconductor industry is sometimes referred to as a knife at China’s heart but also a shield against that knife. However, any forcible move on Taiwan comes with the near-certainty of ruining the very prize China wants. Analysts note that the delicate cleanroom facilities of TSMC could never be operated under military occupation or wartime conditions – the equipment would likely be rendered useless by damage or by sanctions cutting off software, maintenance, and raw materials. Key personnel would flee. In effect, seizing Taiwan’s fabs intact is a nearly impossible task; they are not like capturing an oil well. Even Chinese officials implicitly acknowledge this risk when they lament their dependence on TSMC – a dependence that would not instantly disappear even if they controlled Taiwan geographically [reliance on Taiwanese chips].

Thus, Beijing is walking a tightrope. For now, it benefits from Taiwan’s “silicon shield” as much as the West does, since China’s own tech industries (from electronics manufacturers to AI startups) rely heavily on a steady flow of Taiwanese-made chips. More than half of Taiwan’s semiconductor exports go to China or Hong Kong, feeding factories that assemble everything from iPhones to PCs for global export. Any shock to that flow would hurt China’s economy at least as badly as everyone else’s in the short term. This interdependence has arguably stayed China’s hand, even as nationalist rhetoric about “reunification” grows louder.

However, China’s patience is not infinite. Xi Jinping has tied national pride to technological ascent, and there are internal pressures – economic and political – to show progress and strength. If China’s leadership concludes that peaceful integration or chip self-sufficiency are going nowhere by late this decade, some fear it might consider more drastic action on Taiwan despite the risks. That worst-case scenario is one the world hopes to never see, because it would trigger economic consequences far beyond anything experienced in recent memory.

What would happen if the chips literally went down in Taiwan? It’s a question boardrooms and war rooms alike have been gaming out in recent years. The scenarios range from a military invasion or blockade of Taiwan to natural disasters like a mega-earthquake – anything that could severely disrupt the island’s semiconductor production. The projections are uniformly grim.

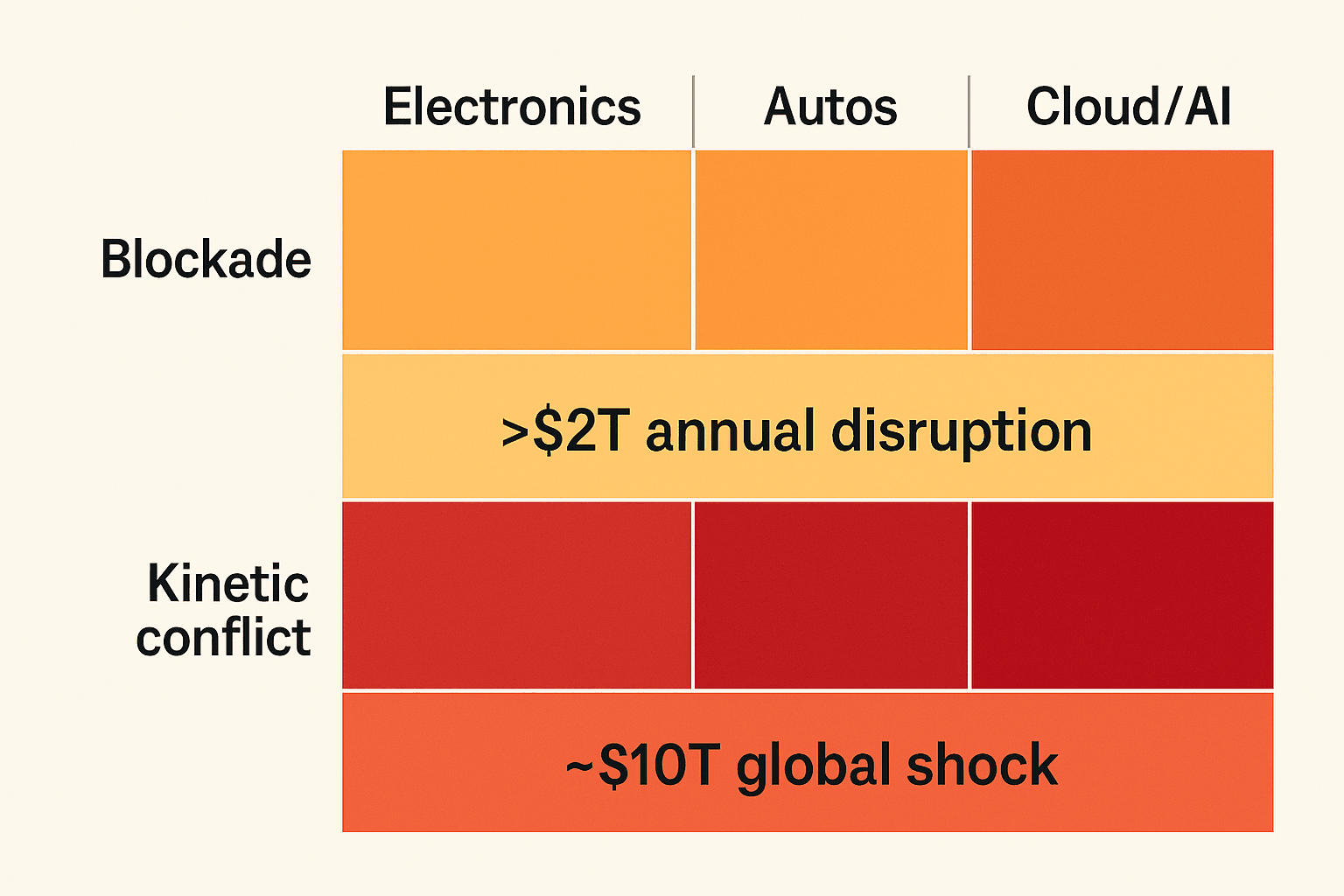

A full-scale China-Taiwan war, in which production halts, would be an economic cataclysm. One analysis by the Institute for Economics and Peace estimated a Taiwan conflict could wipe out over $10 trillion in global economic output. For perspective, that’s several times the impact of the COVID-19 pandemic in a single swoop. Even a less acute scenario, like a Chinese naval blockade that chokes off Taiwan’s trade for a time, could cost the world on the order of $2-3 trillion and plunge economies into recession. The brunt of the pain would fall on Asia – Taiwan’s own economy could shrink 20%, 30%, or more depending on the damage, and China could face a severe contraction due to lost trade and sanctions – but no region would be unscathed. The U.S. electronics industry would grind to a halt for lack of components; European car plants would run out of chips within weeks; global inflation could skyrocket for tech goods.

In short, a hot conflict over Taiwan is viewed as an almost unthinkable worst case for the global economy. This is precisely why many analysts believe it’s unlikely to be allowed to happen. It would simply be too costly for all parties – a textbook example of mutually assured destruction, economically speaking. This reinforces Taiwan’s silicon shield: the very interconnectedness and dependency that make the situation so perilous also act as a deterrent. No one can “win” a chip war that destroys Taiwan’s fabs; the loss would be irreplaceable in the near term.

But “unlikely” doesn’t mean impossible. The mere possibility has sparked urgent efforts worldwide to build contingency plans and resilience. The U.S. military, for instance, has reportedly stockpiled critical chips as a buffer against supply interruption [strengthen microchip supply]. Tech firms have started exploring multi-sourcing strategies (though for cutting-edge chips, alternatives are limited). Governments are conducting risk assessments of critical industries – from defense systems to medical devices – that could be paralyzed by a chip supply shock. In some scenarios, policymakers even consider extreme measures: one infamous academic paper discussed a “scorched earth” strategy where if invasion seemed imminent, Taiwan and the U.S. might deliberately disable TSMC’s facilities to deny them to China. Taiwanese officials have downplayed such ideas, but the fact they are debated underscores how high the stakes have become.

There’s also the question: if Taiwan’s chip output vanished, how quickly could the world fill the gap? In theory, over several years, other producers could expand capacity or new fabs could come online to replace a chunk of the lost output. The U.S., Europe, Japan, and others are positioning themselves to do exactly that – but it would take a long time and huge investment to reach anything near the scale and sophistication Taiwan offers today. In an extreme event, we might witness a rapid reordering of the semiconductor landscape out of sheer necessity. Companies that survive might accelerate efforts to redesign products around whatever chips are available. Governments would invoke emergency laws to prioritize chip supply for critical sectors (much like they did for vaccines in the pandemic). Alliances would be tested: for example, countries might curtail exports of chips to keep their own industries afloat, potentially causing diplomatic rifts.

All these what-ifs serve to highlight a single point: the world cannot afford to let Taiwan’s semiconductor hub go offline without catastrophic consequences. This sobering reality is why maintaining peace and stability in the Taiwan Strait is of global interest, not just a regional issue. It’s also why so much money and effort is now being poured into reducing the risk – essentially buying insurance by diversifying chip production geographically. But until that insurance policy is robust enough, Taiwan’s status as the most critical piece on the global chessboard will persist.

The AI chip war is far from over, and Taiwan will remain at the center of its next chapters. Going forward, several key developments could redefine the balance of power – or the level of risk – surrounding Taiwan’s role:

In conclusion, Taiwan’s central role in the semiconductor ecosystem will remain a defining feature of global geopolitics for the foreseeable future. The island’s “silicon shield” – its mastery of chipmaking – continues to protect it, even as it paints a target on its back. The coming years will test how durable that shield is. Will we see a more balanced global chip supply that lessens the stakes, or an intensification of the chip war as AI and great-power rivalry collide? For investors, executives, and policymakers, staying alert to these tech trends and diplomatic signals isn’t just academic – it’s essential foresight. In the grand chessboard of global power, all eyes remain on that critical square occupied by Taiwan, the small island with an outsized influence on our digital and economic future.

Taiwan (especially TSMC) manufactures the majority of the world’s most advanced semiconductors – over 90% of sub-7nm chips. This means nearly every cutting-edge device or AI system relies on chips made in Taiwan. If Taiwan’s chip production were disrupted, it would create a global tech crisis, affecting smartphones, data centers, cars, and military tech worldwide.

The “silicon shield” is a term for Taiwan’s dominance in semiconductors acting as a deterrent against conflict. Because both China and the West depend on Taiwanese chips, any war over Taiwan could destroy this critical supply and deal a trillion-dollar blow to the global economy. This mutual dependence gives Taiwan a kind of protection – major powers have a strong incentive to avoid disrupting Taiwan’s fabs.

The U.S. and its allies are investing heavily in domestic semiconductor manufacturing. The 2022 CHIPS Act allocated $52B to build fabs in the U.S. (TSMC is building in Arizona, Intel in Ohio, etc.), and countries like Japan, South Korea, and those in Europe are also boosting local production. They’ve also formed informal alliances (sometimes called “Chip 4”) to coordinate these efforts. The goal is to diversify supply so that advanced chips aren’t all made in one place, though catching up to Taiwan’s expertise will take years.

Related reads on TrendDepth: